Tax and accounting requirements in Colombia should be a central part of your market entry strategy to successfully register a company in Colombia and ensure compliance within a complex regulatory environment. This guide provides key insights to help you navigate Colombia’s fiscal regulations effectively. The local tax authority is known as DIAN (Dirección de Impuestos y Aduanas Nacionales) and sets strict rules throughout the territory. This includes not just IFRS reporting but also UBO requirements and so forth aimed at promoting transparency.

Key Takeaways On Tax and Accounting Requirements in Colombia

| What Are The Accounting Standards in Colombia? | Companies in Colombia must comply with International Financial Reporting Standards (IFRS), known locally as NIFF. Accountants must be certified in IFRS. |

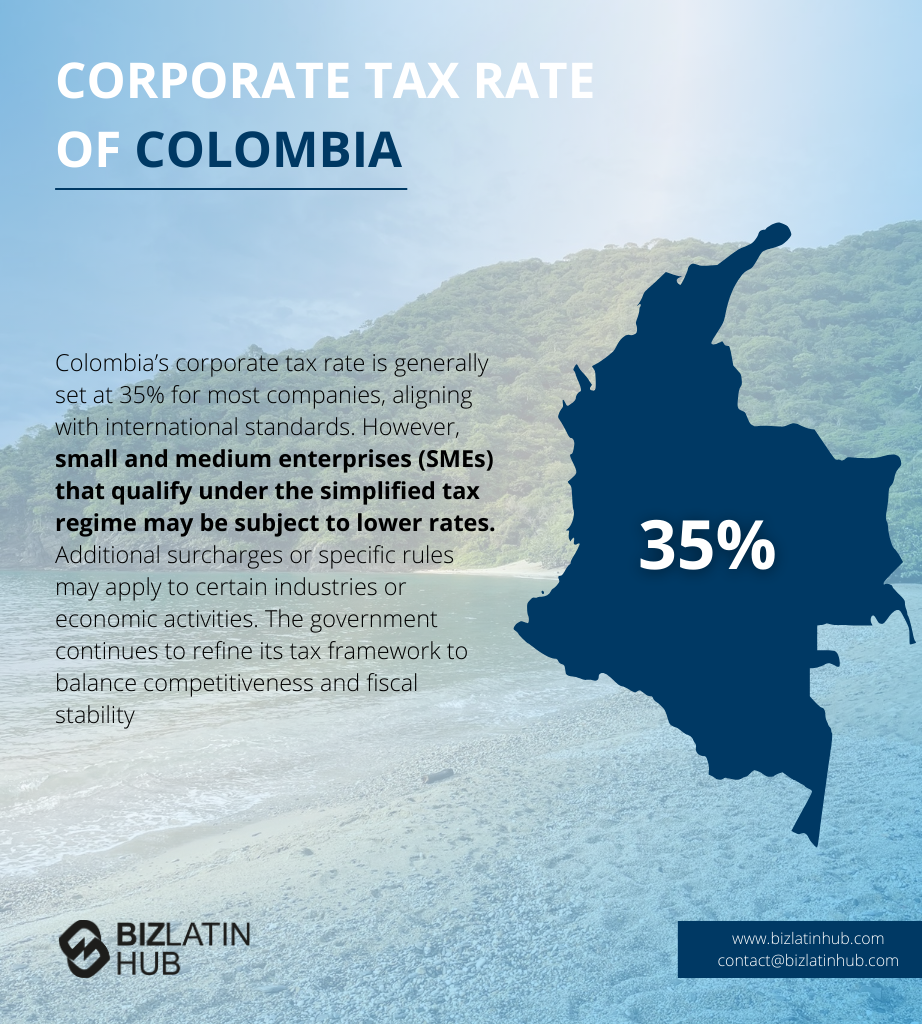

| What Is The Corporate Tax Rate in Colombia? | The corporate tax rate is 35% in Colombia, a high water mark in the region. |

| Colombian Value Added Tax Rate | The current VAT rate (IVA) is set at 17%, with a few variations depending on services and business activity. |

| What is the Dividend Tax Rate in Colombia? | This was increased to 20%, though this might be reduced by effective tax treaties. |

Overview of Colombia’s Tax and Accounting Framework

For most individuals, the mention of accountants immediately brings to mind taxes. Whether you are an individual residing in Colombia or a corporate executive overseeing a multinational operation, understanding Colombian tax laws is crucial to safeguard your interests.

Financial Reporting and IFRS (NIIF) Requirements

All companies operating in Colombia must adhere to International Financial Reporting Standards (IFRS), also referred to as Normas Internacionales de Información Financiera (NIFF) in Spanish. When engaging an accountant in Colombia, ensure they are certified in this process. Compliance is of utmost importance, as fines start at a minimum of a minimum monthly salary, which is roughly equivalent to USD$200. This can amount to up to USD$45,000 in maximum fines, considering the high value of the US dollar.

Doing business in Colombia – double taxation:

Double taxation is not permitted under Colombian law. Colombian tax deductions and calculations differ significantly from those in other countries. The interpretation of allowing US deductions for income earned in the USA varies among Colombian accounting and legal firms. Each individual and company has a unique set of circumstances that should be evaluated by a professional before drawing any conclusions. In some cases, the difference in tax percentages not paid in one country may need to be paid in another.

Corporate Income Tax and Financial Transactions Tax in Colombia

Corporations in Colombia are required to submit monthly tax reports starting from the creation of their first invoice. These reports encompass cash flow statements, as well as monthly, quarterly, and annual reports, ensuring compliance. Payroll (Nominal) mandates monthly reports for employees receiving benefits to maintain compliance. Inactive companies or startups have a minimum filing requirement of quarterly reports, and failing to file results in significant fines imposed by the DIAN (Dirección de Impuestos y Aduanas Nacionales).

In Colombia, it is essential to provide employees with benefits. This applies whether you hire domestic staff or individuals referred to you by acquaintances, working on an hourly basis. Colombian workers expect you to provide their severance pay upon terminating the employment relationship.

Free trade zones in Colombia

Companies operating within an FTZ can access a reduced 20% corporate tax rate, no customs duties for imported goods used in production, and simplified import/export processes. There are over 100 throughout the territory and although every one has its own specifities, the basic rules apply to all. Follow this link from Biz Latin Hub to find out more about free trade zones in Colombia.

What are the Reporting Requirements in Colombia?

Various Colombian government agencies, including the Superintendency of Corporations, the Superintendency of Securities, the Superintendency of Banks, the Tax and Customs Administration, issue regulations and statements on accounting principles. Colombian generally accepted accounting principles (GAAP) are stipulated in decrees. GAAP compliance is mandatory when producing financial statements for any entity involved in income-generating activities in Colombia. These financial statements must provide an accurate depiction of the entity’s financial status, irrespective of tax obligations.

Furthermore, standardized formats must be adhered to when recording any transaction, following the Unique Plan of Accounts (Plan Unico de Cuentas).

Under Colombian corporate laws, accounting records must be maintained in Colombian pesos and in the Spanish language. Non-monetary assets, non-monetary liabilities, and net worth must also be adjusted for inflation and devaluation, using the applicable percentage of adjustment for the fiscal year.

Joint-stock corporations listing their shares on the stock exchange or issuing liabilities, as well as all financial sector entities, must publish their annual financial statements in a local newspaper.

Understanding Colombian Accounting

While fundamental accounting principles are consistent worldwide, Colombian accounting reports and tax laws exhibit notable distinctions. Beyond translating report titles and keywords, experienced Colombian accountants are essential to provide essential information adhering to high standards. For instance, monthly corporate tax filings are mandatory in Colombia, with personal income taxes due in August and September.

Filing deadlines are determined by the last two digits of the corporate ID and the last two digits of the Colombian ID card for personal income tax filings, and these dates can frequently change. To navigate Colombia’s taxation system smoothly, enlisting the assistance of qualified Colombian accountants is crucial.

Accounting Principles and Standards in Colombia

Separate financial statements are not required for corporate income tax purposes in Colombia. Colombian subsidiaries and branches often prepare two sets of financial statements: one for Colombian shareholders and local legal purposes, adhering to Colombian GAAP, and another following the accounting principles generally accepted in the headquarters’ country.

Adjustments used to determine taxable profit are detailed in a tax computation schedule. Companies must prepare financial statements annually for tax purposes, with the calendar year as the standard reporting period. However, certain entities like banks must submit monthly financial statements to the Superintendency of Banks.

IFRS is used in the territory depending on size of company. There are three regulatory groups: Group 1 (large companies and multinationals follow full IFRS), Group 2 (NIIF for SMEs), and Group 3 (simplified accounting).

- Accounting Practices: Basic financial information includes the balance sheet, income statement, statement of retained earnings, statement of changes in shareholder equity, statement of changes in financial position, and statement of cash flows. Notes explaining accounting policies and additional information are integral to the basic financial information.

- Capitalization of interests: Asset costs must include all expenses incurred before the asset’s actual use date. Interest incurred on debts directly related to the asset before its use date should be capitalized. Once the asset is ready for use, interest capitalization ceases.

- Lessee accounting: Lease classification depends on the transaction circumstances, with capital leases as the standard classification. In some cases, leases can be classified as operating leases after meeting specific legal requirements.

- Merger accounting: Assets and liabilities of merged companies are recorded at book value.

- Inventory valuation: Common inventory valuation methods include First-in, first-out (FIFO), last in, first out (LIFO), and weighted-average methods. The methods used for determining ending inventory and the cost of sales include the perpetual inventory system, periodic inventory system, and retail system methods. The standard cost method is acceptable for financial reporting but not for tax law purposes.

- Company dividends: Dividends are registered as a company liability when declared based on previously approved financial statements at the general shareholders’ assembly. Accounting for declared dividends decreases retained earnings and includes dividends in current liabilities.

- Consolidated financial statements in Colombia: The parent or holding company is required to prepare and disclose consolidated financial statements that present the financial position, operational results, changes in net worth, and cash flows of the parent or holding company and its subsidiaries. Investments in non-consolidated subsidiary companies must also be recorded in the parent or holding company’s books using the equity method.

- Unusual items: Unusual items must be disclosed separately in the statement of income. Significant gains or losses resulting from transactions outside the normal course of business are included in this category.

DIAN, UBO, and Compliance Deadlines

DIAN enforces UBO reporting via RUB. Non-compliance leads to monetary sanctions of 100 UVT per day and possible suspension of the RUT (Tax ID), which would effectively prevent operations. Employers are obligated to provide mid-year and end-of-year bonuses (prima), pay contributions to ARL based on risk level, and submit monthly payroll files through DIAN’s electronic payroll platform (Nómina Electrónica).

- VAT returns: monthly, due the 20th–26th of each month depending on NIT.

- Payroll contributions: monthly via PILA by the 10th of the following month.

- Corporate income tax: annual, typically filed between April and August depending on NIT.

- UBO reporting: submitted upon incorporation and updated when ownership changes occur.

Additional FAQs About Tax and Accounting in Colombia

Based on our extensive experience these are the common questions and doubts from our clients when looking to understand accounting and taxation in Colombia.

1. What is the corporate tax rate in Colombia?

The corporate tax rate in Colombia is 35%.

2. How are businesses taxed in Colombia?

Companies in Colombia are taxed on income.

3. What is the IRS called in Colombia?

The IRS in Colombia is called the DIAN – National Directorate of Taxes and Customs.

4. What is the accounting standard in Colombia?

Colombian accounting standards include IFRS (International Financial Reporting Standard), known as NIFF (Normas Internacionales de Información Financiera) in Spanish, the National Tax Statute, and Decree 2649 of 1993, which mandates generally accepted accounting principles (GAAP) as accounting standards. Financial statements must be prepared in Spanish, and bookkeeping must also be in Spanish.

5. What is the CPA equivalent in Colombia?

The equivalent of the CPA in Colombia is the Junta Central de Contadores.

6. Does Colombia report in IFRS?

Yes. All Colombian companies must comply with NIIF (IFRS), grouped into three categories:

Group 3: Small entities use a simplified accounting framework.

Annual financial statements must be submitted to the Chamber of Commerce and, in some cases, the Superintendence of Companies.

Group 1 (NIIF Plenas): Large companies and listed entities.

Group 2 (NIIF para PYMEs): Medium-sized enterprises.

7. What is the corporate tax rate in Colombia for 2025?

The standard corporate income tax rate in Colombia is 35%. Companies operating in Free Trade Zones may benefit from a preferential 20% rate. Some sectors, such as banking and hydrocarbons, may be subject to surcharges.

8. What is the VAT rate in Colombia and how often must it be filed?

The VAT (IVA) rate in Colombia is 19%. Businesses must file VAT returns monthly and issue electronic invoices in accordance with DIAN regulations. VAT refunds are available for exporters under specific procedures.

9. What are the payroll tax obligations in Colombia?

Employers must contribute approximately 30% of an employee’s salary to health, pension, labor risk insurance (ARL), and other funds (e.g., ICBF, SENA, Family Compensation Fund). Employees contribute around 8%. Payroll filings must be submitted monthly through PILA (Planilla Integrada de Liquidación de Aportes).

10. What is UBO registration and is it mandatory in Colombia?

Yes. All companies must register their Ultimate Beneficial Owner (UBO) with DIAN through the RUB (Registro Único de Beneficiarios Finales). The information must be kept up to date, and failure to report can result in daily fines of up to 100 UVT (approx. COP $4 million) per day.

11. What is the financial transactions tax (GMF) in Colombia?

The GMF, or “4×1000” tax, is a 0.4% levy applied to all withdrawals and transfers made from Colombian bank accounts. It is automatically withheld by financial institutions.

Why Invest in Colombia?

Colombia presents a strong investment opportunity due to its robust economic growth, strategic location, and abundant natural resources.

As a leading producer of coffee, flowers, and oil, the country is also seeing increasing potential in sectors such as renewable energy, infrastructure, and technology. Its geographic positioning as a bridge between North and South America enhances its importance in global trade.

Economic reforms, improved security, and a focus on attracting foreign investment have strengthened Colombia’s business environment.

Free trade agreements, competitive labor costs, and government incentives for sectors like tourism and agribusiness further bolster its appeal.

With a skilled workforce and access to key global markets, Colombia offers significant potential for business growth and investment.

How can Biz Latin Hub help you with tax and accounting requirements in Colombia?

If you do not have all the documentation and know exactly how to fill in corporate tax reports you don’t really need an accountant. Yet the Colombian taxation system can have its complications and can end up being a great source of stress and time loss. Completing the return outside of the established dates can lead to large penalties.

If you have any questions or need help completing your fiscal auditing, internal audit or you need advice in analyzing budgets and forecasts before starting up in Colombia, contact Biz Latin Hub. Our team of accountants in Colombia can help you with your tax reporting through the provision of tailored and affordable accounting services. Contact us now for more information.

If you want to learn about the opportunities of doing business in Colombia, check out this video: