Accounting and taxation in Honduras is a key component of your market entry strategy, helping to ensure when you incorporate a company in Honduras it reamins compliant with the country’s regulatory framework. Biz Latin Hub provides specialized support in navigating Honduras’ accounting standards. Honduras’s tax system is managed by the SAR, while payroll and social security are regulated by IHSS (health), RAP (housing), and INFOP (training fund). This guide details the specific fiscal obligations supervised by the Revenue Administration Service (SAR), including income and asset-based taxes.

Key Takeaways On Accounting and Taxation in Honduras

| What Are The Accounting Standards in Honduras? | Honduran accounting standards mandate that companies prepare their financial statements in Spanish, following International Financial Reporting Standards. Accounting records and books must also be maintained in Spanish. |

| What is the standard Corporate Income Tax rate? | The tax rate for a resident company is 25% of its net taxable income. |

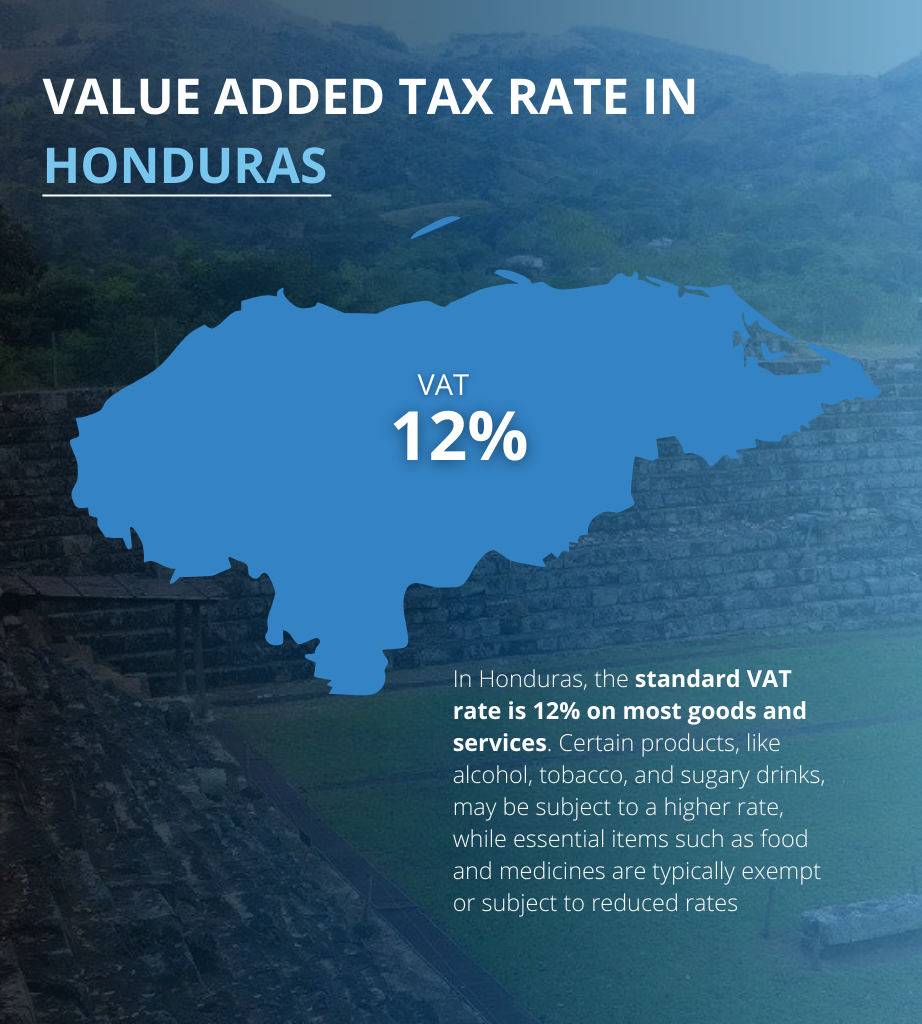

| What Is The Honduran Value Added Tax Rate? | The VAT (IVA) rate in Honduras is set at 15% |

| Dividend Tax Rate in Honduras | A withholding tax is paid at 10% in Honduras. |

| What is the Net Assets Tax? | This is a 1% levy on the value of all assets held by the company and must be paid regardless of profitability. |

Thinking of starting a business in Honduras? Here are some essential points about the Honduran corporate tax regime to keep in mind:

- Territorial Income Principle

- Resident vs. Non-Resident Taxation

- Municipal Taxes

- Withholding Tax on Non-Residents

- Taxation of Companies with Shareholders

- Territorial Income Principle: In Honduras, tax liability is based on the Principle of Territorial Income. This means that individuals and entities are taxed only on income generated from Honduran sources.

- Resident vs. Non-Resident Taxation: The tax treatment varies for resident and non-resident companies. Resident companies are subject to a progressive income tax rate of up to 25%. Non-resident businesses are taxed on their Honduran-sourced gross income at rates ranging from 10 to 25%, depending on their business activities.

- Municipal Taxes: Businesses operating within a municipality in Honduras are subject to municipal taxes. Each municipality has its formula for calculating these taxes, and some may offer tax incentives.

- Withholding Tax on Non-Residents: The Revenue Administration Service (SAR) enforces a withholding tax on non-resident entities receiving dividends, interest, rents, royalties, or management fees from a Honduran company or a foreign business based in Honduras.

- Taxation of Companies with Shareholders: Companies in Honduras, including branches of foreign businesses, can have both resident and non-resident shareholders, quota holders, or directors. The company’s location in Honduras does not affect its income tax obligations.

When forming a company in Honduras, navigating the laws, rules, and requirements of a new jurisdiction can be daunting. That’s why when it comes to accounting and taxation in Honduras, it is best to seek local accountancy and legal professionals to help make the incorporation process as painless as possible.

Corporate Income Tax (ISR) and Dividend Withholding

In Honduras, companies are subject to specific tax rates crucial for compliance and financial planning. Here’s a breakdown of the key taxation elements:

- Corporate Income Tax: Businesses operating in Honduras must pay a corporate tax of 25% on their annual taxable income.

- Additional Surtax for Higher Earnings: For business entities with an annual taxable income exceeding HNL$1.13 million (approximately USD$46,000), there is an additional surtax of 5%.

- Alternative Minimum Tax: Companies with an annual gross income of HNL$11.3 million (USD$460,000) or more are subject to an alternative tax rate of 1.5%. This underscores the importance of having a proficient accounting and taxation team in Honduras to ensure adherence to these regulations.

- Tax on Investment Income and Capital Gains: Income from investments and capital gains in Honduras are taxed at a rate of 10%.

- Dividends and Interest Tax: A 10% tax is applied to dividends and interest payments to foreign companies when the income is from Honduras.

Expert Tip: The Asset Tax as a Minimum Tax

From our experience, the Net Assets Tax is often a surprise for businesses reporting a loss. This is a 1% tax on the company’s total assets (minus certain allowances). Crucially, it acts as an alternative minimum tax. You calculate both your Income Tax (on profit) and your Asset Tax. You pay whichever is higher. This means that even if your company makes zero profit in a year, you may still have a significant tax liability based on the value of your assets. We advise asset-heavy companies to plan cash flow accordingly.

Sales Tax (ISV), Filing Frequency, and SAR Rules

The Impuesto Sobre Ventas (ISV) or VAT is 15%, with a increased rate of 18% on certain luxury goods. ISV returns must be filed monthly through the SAR’s online portal by the 10th. Electronic invoicing is mandatory for large taxpayers and is being extended to other categories. Corporate tax returns are due by April 30 annually. Payroll contributions must be submitted monthly, and the 13th salary is due in December.

Payroll Contributions: IHSS, RAP, and Income Tax

7.08% to IHSS (health)

2% to RAP (housing fund)

1.5% to INFOP (training)

Employees contribute 2.5% to IHSS and 1.5% to RAP. Monthly filings must be submitted to each fund and to the SAR for tax withholdings. The minimum wage and holiday bonus (aguinaldo) must also be paid as per labor laws.The Role of the SAR7.08% to IHSS (health)

2% to RAP (housing fund)

1.5% to INFOP (training)

Employees contribute 2.5% to IHSS and 1.5% to RAP. Monthly filings must be submitted to each fund and to the SAR for tax withholdings. The minimum wage and holiday bonus (aguinaldo) must also be paid as per labor laws.

Financial Reporting and UBO Requirements

Yes. Companies must prepare financial reports annually and retain books in Spanish using authorized accounting software or ledgers. Some sectors, like banking or telecom, must submit reports to regulatory entities. All taxpayers are subject to audit by SAR.

Companies must register a RUC (Registro Único de Contribuyentes) with SAR upon incorporation. Ultimate Beneficial Owners (UBOs) must be disclosed and kept updated within 30 days of any ownership change under anti-money laundering laws. Non-compliance may lead to fines and cancellation of tax registration.

The Role of the SAR

The Revenue Administration Service (Servicio de Administración de Rentas – SAR) is the Honduran tax authority. Companies must obtain a National Tax Registry (RTN) number and file returns through the SAR’s online platform.

Free Trade Zones: Do accounting and taxation regimes in Honduras still apply?

The standard accounting and taxation regimes differ significantly in Honduras, Free Trade Zones (FTZs). Honduras offers 39 FTZs, including 24 privately operated ones, primarily to encourage growth in commercial, manufacturing, and tourism.

Companies operating in these zones, which commonly include textile manufacturers, sporting goods producers, electronics assemblers, auto parts manufacturers, agribusinesses, and tourism companies, benefit from substantial tax exemptions. However, to operate in an FTZ, businesses must obtain approval from the Honduran Ministry of Economy.

Here are the primary tax exemptions available to businesses in Honduran FTZs:

- Import Tax Exemption: Normally as high as 20%, this tax is waived for companies in FTZs.

- Profit Tax Exemption: Businesses enjoy a 10-year exemption from taxes on profits earned from the sale of goods outside of Honduras.

- Income Tax Exemption: Both national and municipal income taxes are waived for 10 years for companies in FTZs.

- Sales Tax (VAT) Exemption: Companies are exempt from VAT, which typically ranges between 15-18%.

- Tourism Sector Benefits: Businesses in the tourism sector operating within a Honduran Tourism Zone are exempt from import taxes, VATs, and income taxes.

- Tax-Free Currency Exchange: Companies in FTZs benefit from tax-free currency exchange.

These incentives make FTZs attractive for foreign and local businesses looking to reduce their tax burden and simplify their accounting processes in Honduras.

FAQs when understanding accounting and taxation in Honduras

Based on our extensive experience these are the common questions and doubts from our clients when looking to understand accounting and taxation in Honduras.

The general corporate income tax (ISR) rate is 25%, plus a 5% solidarity contribution, resulting in an effective rate of 30%. Companies must file annual returns via the SAR (Servicio de Administración de Rentas). Dividend distributions are subject to a 10% withholding tax. All businesses must maintain formal accounting records.

In Honduras, companies are subject to specific tax rates crucial for compliance and financial planning. Here’s a breakdown of the key taxation elements:

Corporate Income Tax: Businesses operating in Honduras must pay a corporate tax of 25% on their annual taxable income.

Additional Surtax for Higher Earnings: For business entities with an annual taxable income exceeding HNL$1.13 million (approximately USD$46,000), there is an additional surtax of 5%.

Alternative Minimum Tax: Companies with an annual gross income of HNL$11.3 million (USD$460,000) or more are subject to an alternative tax rate of 1.5%. This underscores the importance of having a proficient accounting and taxation team in Honduras to ensure adherence to these regulations.

Tax on Investment Income and Capital Gains: Income from investments and capital gains in Honduras are taxed at a rate of 10%.

Dividends and Interest Tax: A 10% tax is applied to dividends and interest payments to foreign companies when the income is from Honduras.

The IRS in Honduras is called the Secretaría de Finanzas (SEFIN) and it is responsible for implementing the fiscal and customs legislation in Honduras.

Honduran accounting standards require companies to prepare their financial statements in Spanish and according to International Financial Reporting Standards. Accounting registries and books of account must be recorded in Spanish.

The equivalent of a CPA in Honduras is a certified public accountant (Contador Publico Autorizado—CPA).

All listed companies must follow IFRS Standards.

The Impuesto Sobre Ventas (ISV) or VAT is 15%, with a increased rate of 18% on certain luxury goods. ISV returns must be filed monthly through the SAR’s online portal. Electronic invoicing is mandatory for large taxpayers and is being extended to other categories.

Employers must contribute:

7.08% to IHSS (health)

2% to RAP (housing fund)

1.5% to INFOP (training)

Employees contribute 2.5% to IHSS and 1.5% to RAP. Monthly filings must be submitted to each fund and to the SAR for tax withholdings. The minimum wage and holiday bonus (aguinaldo) must also be paid as per labor laws.

Companies must register a RUC (Registro Único de Contribuyentes) with SAR upon incorporation. Ultimate Beneficial Owners (UBOs) must be disclosed and kept updated under anti-money laundering laws. Non-compliance may lead to fines and cancellation of tax registration.

Yes. Companies must prepare financial reports annually and retain books in Spanish using authorized accounting software or ledgers. Some sectors, like banking or telecom, must submit reports to regulatory entities. All taxpayers are subject to audit by SAR.

Corporate tax returns are due by April 30 annually. ISV filings are monthly by the 10th. Payroll contributions must be submitted monthly, and the 13th salary is due in December. UBO updates must be filed within 30 days of any ownership change.

This is an additional 5% surtax applied to taxable income that exceeds HNL 1,000,000. It effectively raises the tax rate to 30% for larger profits.

Why Invest in Honduras?

Honduras offers a growing economy with key sectors such as agriculture, manufacturing, and tourism. The country has a strategic location in Central America, providing easy access to both North and South American markets. Its relatively low labor costs and investment incentives make it an attractive destination for foreign businesses looking to expand.

The government of Honduras has worked to improve infrastructure, including ports, roads, and telecommunications. These developments support business operations and enhance trade opportunities. Additionally, the country’s rich natural resources, including minerals and fertile land, present opportunities in mining and agriculture, further driving economic potential.

Biz Latin Hub can help you with accounting and taxation in Honduras

Honduras offers many attractive benefits for those looking to establish business operations in the region. Taking the time to understand the local tax and accounting requirements and ensuring that you have a solid support network of legal and accounting staff can be crucial to the success of your business.

Biz Latin Hub is the market leader in helping local and foreign companies to successfully expand their business in Honduras by providing a full suite of multi-lingual commercial representation and back-office services.

To learn more about the Honduran economy and the business opportunities to form a company in Honduras, please contact us today.